In early 1999, two students raised $100,000 to turn a research idea into a company. Young and risk-averse, they approached the market leader asking to be bought for $1 Million. They were negotiated down to $750,000 before the market leader finally decided not to make the purchase. The small startup asking to be acquired? Google, which IPO’d in 2004 and currently has a market cap of $192 Billion. The market leader that turned down the acquisition? Excite, which would merge with @Home Network before filing for bankruptcy in 2001.1

Besides being an example of perhaps the worst business decision ever made, this story illustrates the uncertainty and difficulty in making acquisition and IPO decisions. When a startup2 is founded and raises capital, the investors are looking for an eventual liquidation event in order to get a return on their investment. Startups essentially have two options for a positive liquidation event: Acquisition or IPO.3 Most startups nowadays (like Google in ‘99) are aiming for an acquisition- to be bought by a tech giant and hopefully have the product incorporated. Popular Google products like Adsense and Android are based on acquisitions of Applied Semantics and Android Inc. respectively. However, acquired products often fail, like the location based service Dodgeball, founded by Dennis Crowley and bought by Google in 2005. Google failed to properly integrate it and closed the service in 2009. Dennis Crowley went on to use his Google money to found FourSquare.

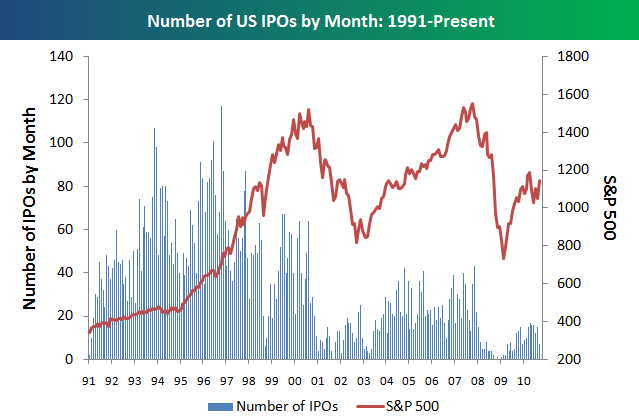

It is rare in the current startup ecosystem to hear of a startup aiming for an IPO. The Initial Public Offering (IPO) means that the company will begin selling its shares to the public, i.e you can buy it on the stock market just like Microsoft(MFST) or Apple(AAPL). In the late ’90s, the mismanagement and failure of companies like Excite, Pets.com, and Go.com led to the crash of the Dot-com bubble. This crash was followed by the Enron and WorldCom scandals of the early 2000’s. These systemic failures led to the increased scrutiny of the public markets and eventually the passage of Sarbanes-Oxley.4 A combination of the difficulties of compliance under Sarbanes-Oxley and vestigial negative perception of IPOs has caused the number of startups going public to be significantly smaller than in the past. (See graph below) Behemoth companies like Facebook (with over 3,000 employees) are still choosing to forgo IPO and rely on outside financing.

IPO vs S&P

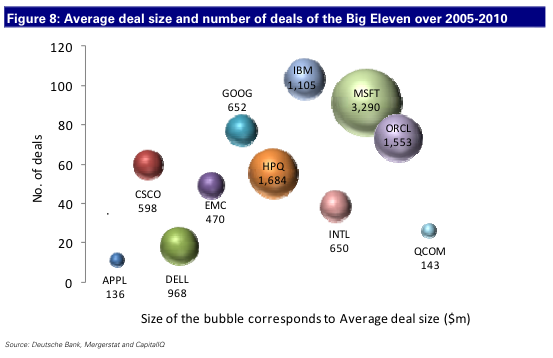

Seemingly following the trend away from IPO, Groupon recently began talks with Google to be acquired for just over $5 Billion.5 However, these talks fell through for a number of reasons. I am impressed by Groupon’s board’s decision to turn down this offer and continue their aggressive expansion strategy by raising more investment.6 I believe that the pendulum has swung too far against startups seeking IPOs and think that Groupon’s decision to go it alone will be greatly beneficial to the startup ecosystem, as well as overall technological innovation. As explained above, most successful innovative startups will be acquired by tech giants looking to incorporate their technology into their offerings. Currently, there are not too many tech giants with major acquisition budgets, creating a small oligopoly of purchasers available to desirable startups (see chart below). If companies like Groupon, Facebook, and Twitter decide to go the IPO route they can join these big acquirers in spurring innovations via acquisitions.

Tech Acquirers

Think about how different the world would be today if Excite had decided to buy the barely formed Google in ‘99. How many times a day do you “Google" something? How much collective time does the world save by getting the incredible results of Google? If Excite hadn’t made their boneheaded decision we would not have one of the most innovative companies to ever exist, one that is currently tackling such big problems as renewable energy and creating such innovations as self-driving cars. So, thank you Groupon for choosing not to be acquired! Follow the lesson of Larry and Sergey, and let’s see what Groupon is in 10 years.

-

When Google Wanted to Sell to Excite for Under $1 Million (TechCrunch) ↩︎

-

I am referring to tech startups that are aggressively growing with the intent of being “The Next Big Thing.” Not a small/lifestyle business ↩︎

-

Not including mergers for simplicity ↩︎

-

Worst Ideas of the Decade: Sarbanes-Oxley (washington Post) ↩︎

-

Here’s Google’s Real Offer For Groupon (Business Insider) ↩︎

-

Groupon Closing $950 Million Round, Valued At $4.75 Billion ↩︎